Commercial real estate trends are driving and being driven by technology on both the business side and the consumer side.

Recent years have seen a ramping up in customer demand when it comes to technology, where they are more frequently opting to favor digital experiences as opposed to traditional ones—businesses have had to meet this demand.

The National Association of Realtors’ 2019 Profile of Real Estate Firms found that 44% of commercial real estate companies said keeping up with technology was one of the biggest challenges they will face in the next two years. The only factor that ranked higher was local or regional economic conditions (46%).

Today, we’re going to be laying out the biggest commercial real estate trends and challenges that are facing businesses today.

1. Augmented Reality

Augmented reality in real estate means allowing customers to tour properties using nothing more than their phone.

AR superimposes an image for the user, allowing the them to move the device and “project” the property onto a surface.

Far from a technological gimmick, AR is an extremely useful tool for realtors and potential buyers for a number of reasons, namely:

- It offers a much greater and more tangible view than a standard photo is able to convey

- Realtors can’t photograph everything, and as such users may not be able to see exactly what they want—AR addresses this

- Physical tours are time-consuming for buyers

Of course, we’re not suggesting that AR will replace physical visits by any means. Buyers will more often than not want to view a property before making any kind of meaningful decision.

However, for properties that have grabbed their attention, but visual resources haven’t been enough for them to arrange a viewing; this is the kind of scenario where AR can act as a useful introduction to a property to further interest.

64.4% of apartment buyers confirm that 3D- and VR-content helps to “feel” the real size and volume of rooms of housing.

2. Online Accessibility

Consumers expect quality digital experiences in virtually every walk of life, whether it’s banking or ordering takeout pizza—and real estate is no exception.

Users research, buy, sell, and rent; all online. It’s up to real estate businesses to be there for them and help them through the process.

This includes connecting with them through social media channels and being diligent in your response times to them.

Realtors must consider a few things in their approaches to their online accessibility:

- 99% of millennials and 90% of baby boomers begin their searches for a new home online.

- 77% of realtors actively use social media for real estate in some way, shape or form.

- 47% of real estate businesses note that social media results in the highest quality leads versus other sources.

What’s notable here is that while realtors appear to understand how important their online presence is, nearly a quarter of them aren’t active on social media.

How active is your business on your online channels?

3. The iBuyer Model

“iBuyers” are a relatively new trend that’s been developing in commercial real estate.

The basic concept is that an iBuyer is a person or company who uses algorithms to buy and sell properties in a matter of days.

The realtor buys the property at a reduced price, then re-sells it on the open market—though that may sound eerily familiar to flipping, realtors avoid selling the service as such.

The trend has picked up in recent years primarily as a result of homeowners wanting to avoid the typical months- or years-long delays in selling a house, in addition to moving-out and moving-in times which are always tricky pain points.

In Q3 2019, iBuyers bought 3.1% of all homes purchased across 18 markets in the US, up from 1.6% the previous year.

It’s still an emerging market, but recent growth indicates that there is certainly a place for it for people who need it, and traditional realtors are getting in on the action too by educating themselves about the options sellers have, and in some cases even representing them as a broker to iBuyer companies.

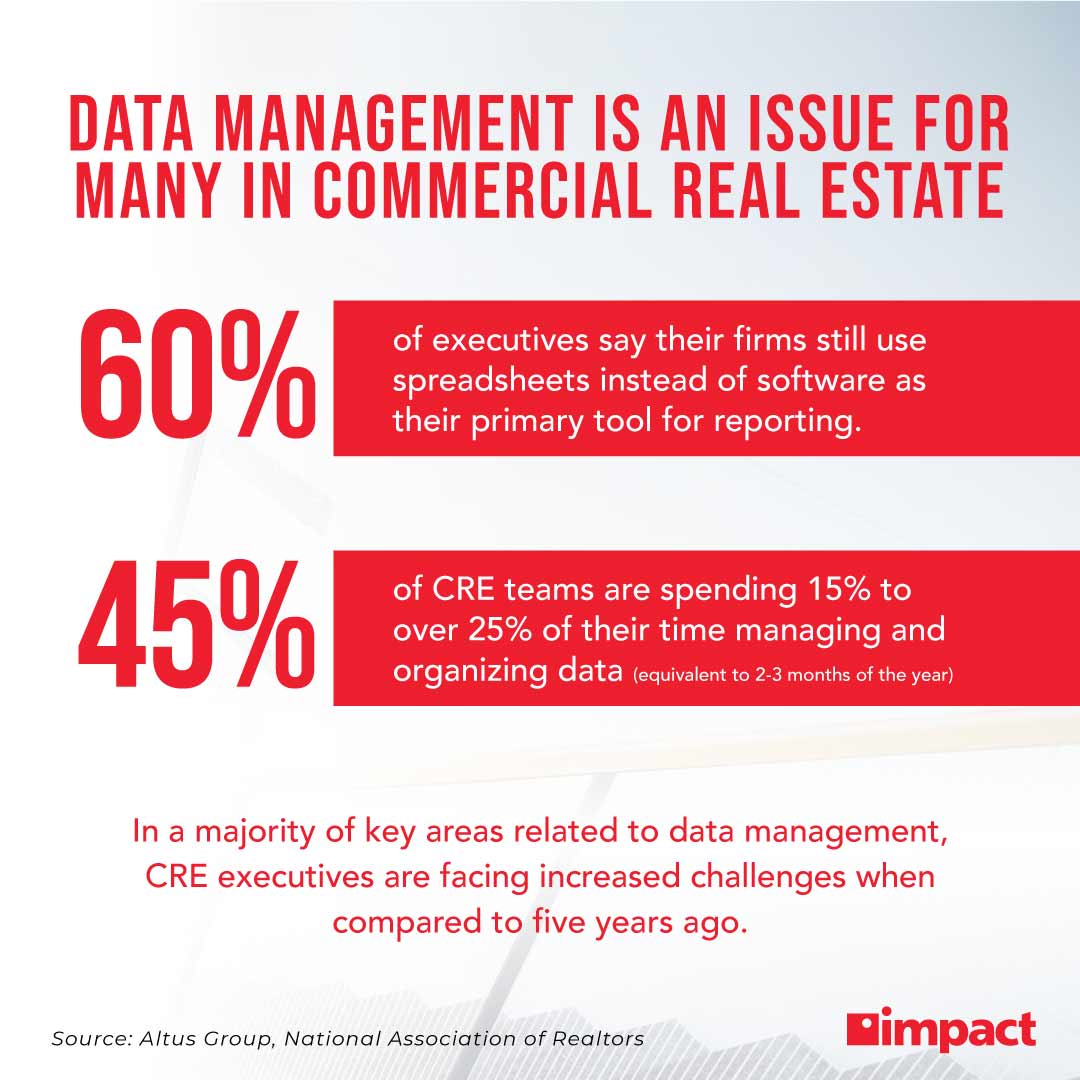

4. Big Data

Data is as important to realtors, developers, and investors as it is to anyone in any other industry.

Just like any asset, identifying trends and having the ability to use digital tools to gain actionable data is vital. Being slow in decision-making is not an enviable attribute for any business.

This is where big data has emerged as one of, if the not the key trend of the last 10 years.

Machine learning and automated algorithms which can independently crawl, aggregate, and interpret data are becoming more commonplace than ever, and organizations should look to make use of these tools and implement them sooner rather than later.

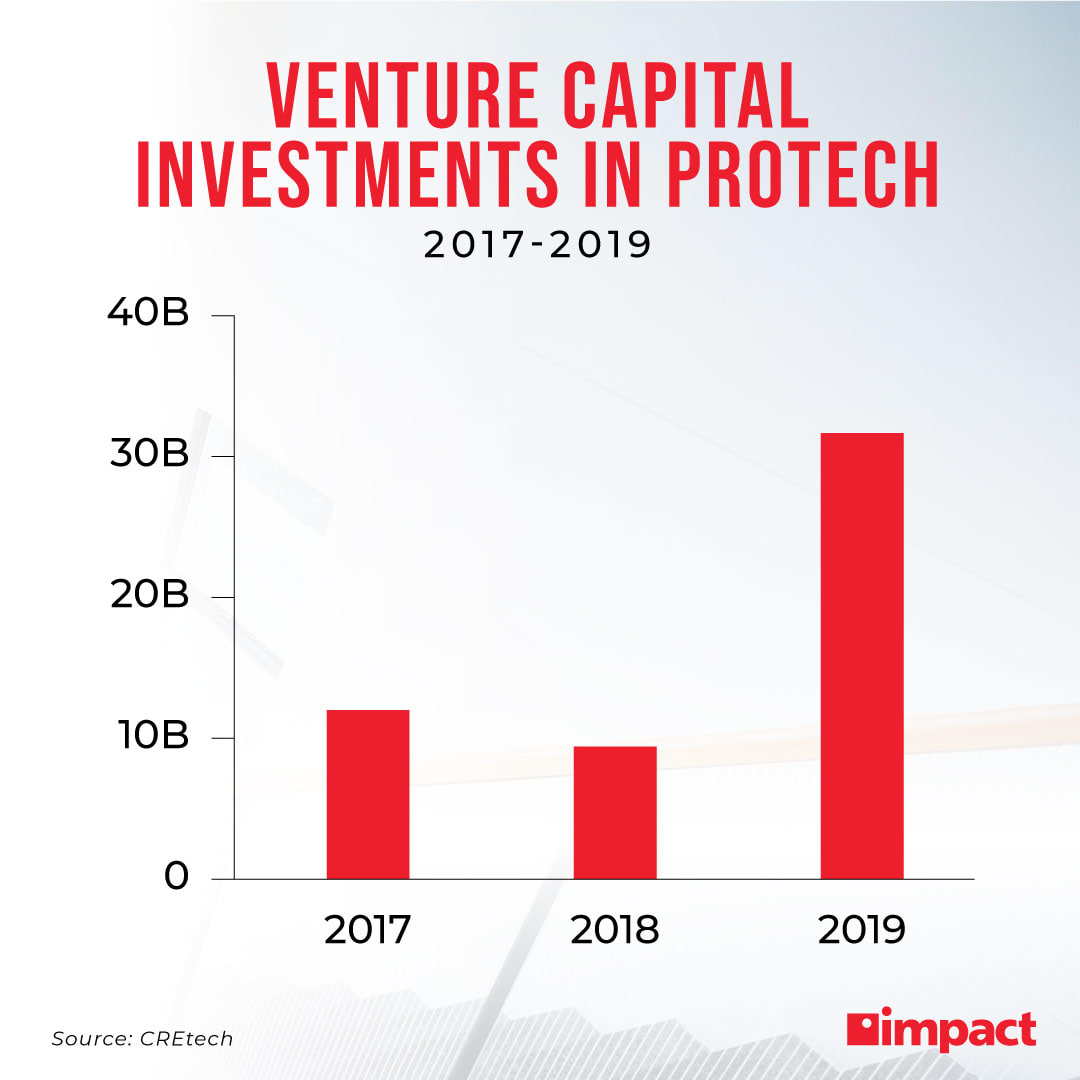

5. PropTech

PropTech (short for property technology) is a relatively new and confusing buzzword that has been in a commercial real estate trend for a number of years, now.

In an effort to save confusing the matter further, PropTech essentially boils down using technology to approach real estate from a new angle.

This, of course, manifests itself in several ways that will be familiar to most people who have moved somewhere new recently, and indeed all of the above trends are examples of PropTech.

It is, in laymen’s, the biggest disruptor in the industry. Typical proponents will be companies that are tech-focused, and products of PropTech are more often than not an app or service like iBuying that disrupts an existing traditional method in real estate.

Affordability, long leasing and buying processes, and digital flexibility are all examples of pain points that PropTech organizations hope to solve.

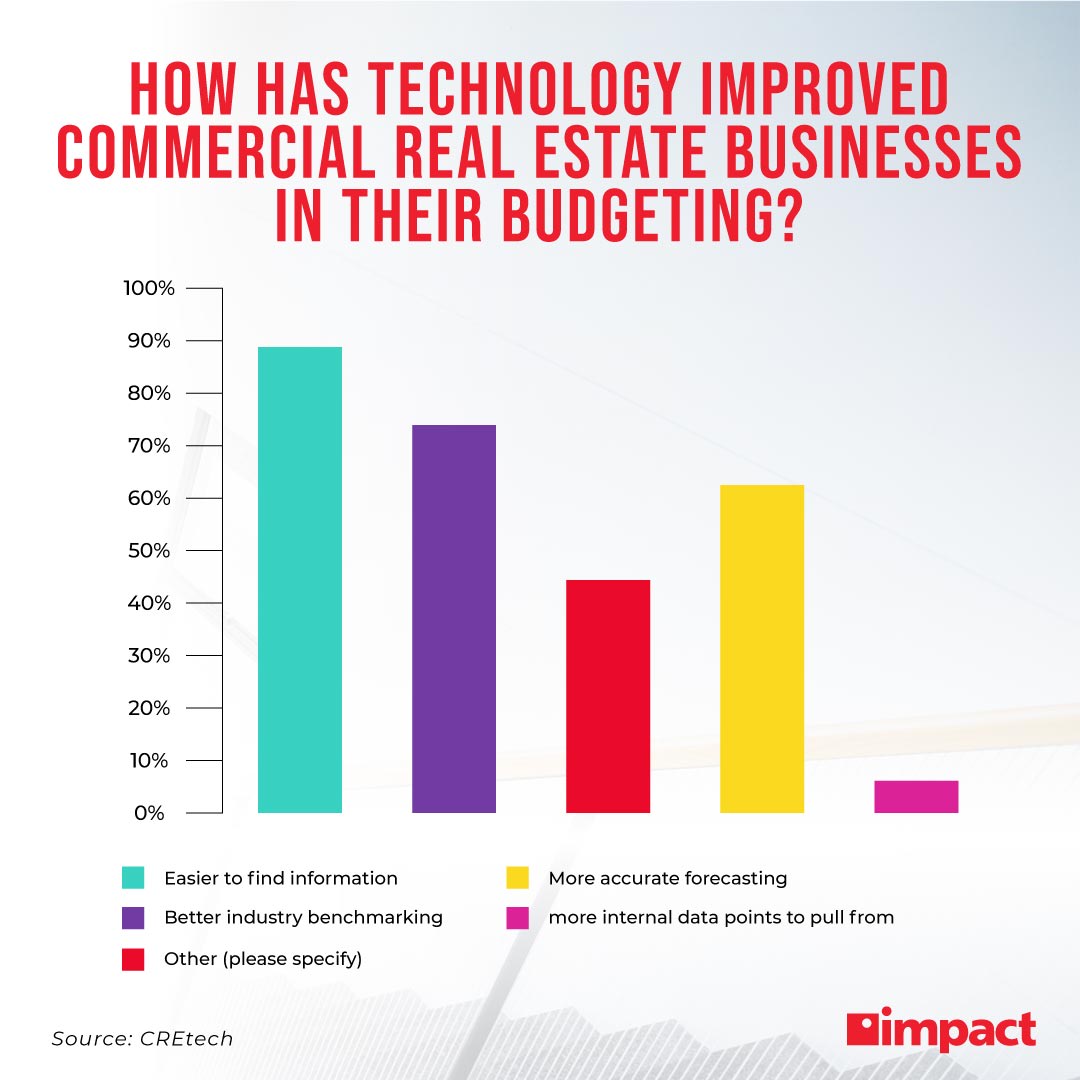

6. Digital Platforms

One of the more innocuous but nevertheless vital uses of PropTech is this next trend—the use of digital platforms by realtors to improve their work processes and streamline their business expenses.

The most familiar ways of doing this are usually through automating manual processes and using software to digitize paper-based tasks.

An obvious example of this is a document management solution like DocuWare, which can scan and digitize paper documents with verifiable e-signatures from customers.

The simple implementation of a digital platform like this is a boon for SMBs looking to cut costs, not just in terms of money, but time too.

On average, it takes 37 minutes to receive a signed document with the electronic signature. By the traditional route, the process could take up to 5 days or more.

In commercial real estate, time is sensitive, so it’s no surprise that businesses are clamoring for solutions to digitize their everyday processes—it’s the major reason the market for management software in real estate is expected to hit $12.9 billion by 2025.

7. Tech Adoption Is Relatively Slow

In spite of all these commercial real estate trends, there is one that should be noted by organizations in the industry—and that being that many businesses are slow to implementing technology.

As with most industries, frontrunners—those who have adopted technology early—often end up being the biggest beneficiaries of changing markets.

And while the majority of organizations in real estate accept that they will have to adopt a digital strategy, there appears to be a large gulf between the sayers and doers.

KPMG’s 2018 Global PropTech Survey found that 66% of real estate decision-makers say they have not implemented a digital and technological innovation vision or strategy at their firms.

We’ve already seen the impact that PropTech is having on the industry, and the consensus of business leaders accepting that digital innovation is their biggest challenge, but those actually formulating and carrying out plans for digitization have generally lagged behind frontrunners.

Recent indications, however, suggest that more SMBs are taking this to heart by investing more in technology.

For example, 8 out of 10 commercial real estate businesses now employ a Chief Data Officer to oversee the organization of their data strategy and governance—a large increase from four years ago, when 44% of companies lacked such a role.

So while adoption is slow, the growing sense within the industry is that technology strategies are necessary and essential, and we expect adoption to increase rapidly with the rise of PropTech initiatives and other major disruptors in the real estate landscape.

Know that you need digital solutions but don’t know where to start? Don’t worry, you’re not alone; digital transformation is complex. To find out more about business cloud technology and which solutions are right for keeping your business competitive and in good shape for the future, download our eBook, “Which Cloud Option Is Right For Your Business?”